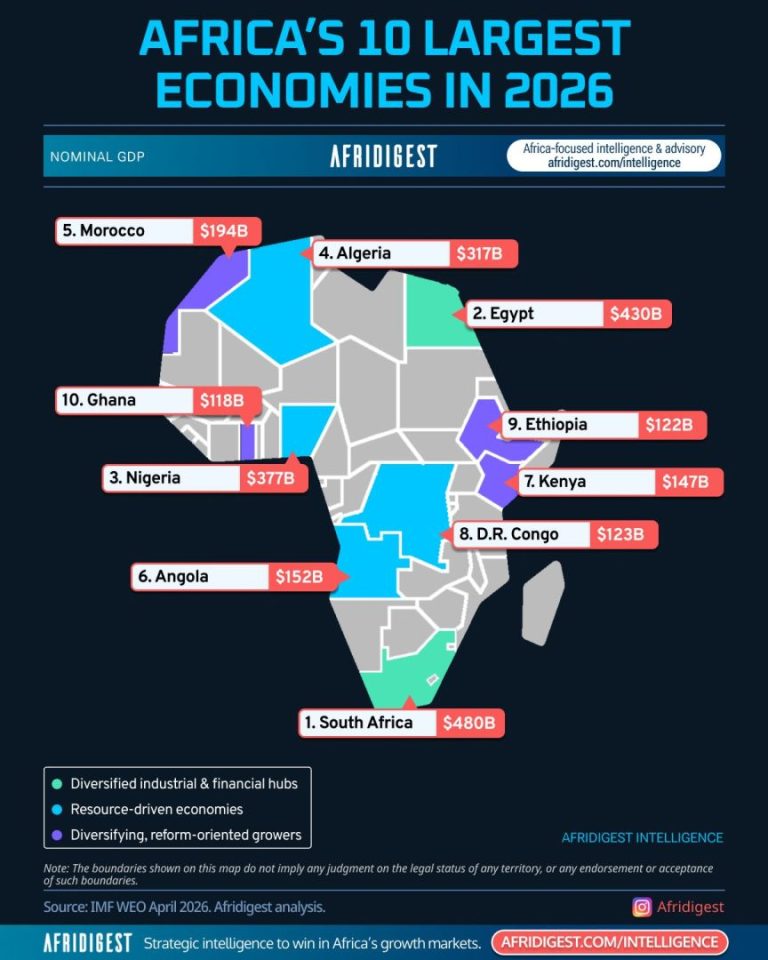

Africa’s 10 largest economies in 2026 account for roughly 70% of Africa’s total $3.6 trillion GDP.

These continental powerhouses can be split into 3 groups:

- Diversified industrial & financial hubs (🇿🇦, 🇪🇬) with deep capital markets and industrial bases built over decades, but that are now facing the harder problem of reigniting growth

- Resource-driven economies (🇳🇬, 🇩🇿, 🇦🇴, 🇨🇩) whose outlook is largely dependent on oil or minerals, with diversification still more aspiration than reality

- Diversifying, reform-oriented growers (🇲🇦, 🇰🇪, 🇪🇹, 🇬🇭) that are in the middle of building the institutions and industries that compound over time

Here’s an overview of each economy:

- South Africa – $480B – diversified industrial & financial hub – diversified industry, the continent’s deepest capital markets, advanced financial infrastructure; but constrained by persistent energy challenges, high unemployment, and sluggish growth.

- Egypt – $430B – diversified industrial & financial hub – a large and young domestic market, strategic geography bridging Africa and the Middle East, significant infrastructure investment; but working through IMF-backed reforms and currency stabilization.

- Nigeria – $377B – resource-driven economy – Africa’s most populous nation has experienced a windfall from increased global crude oil prices; but severe domestic inflation, currency depreciation, and macro instability have compressed its nominal GDP. The gap between its demographic weight and economic size is one of the defining tensions in African business today.

- Algeria – $317B – resource-driven economy – Europe’s third-largest gas supplier, a position that’s gained strategic weight given the Middle East conflict’s disruption to other energy routes; oil and gas still account for ~20% of GDP and over 85% of export revenue; diversification into manufacturing and agriculture remains gradual.

- Morocco – $194B – diversifying, reform-oriented grower – one of Africa’s most diversified, export-oriented economies: the automotive and aerospace manufacturing hub of the continent, the world’s largest phosphate reserves (~70% of global supply), and Tanger Med, among the most efficient container ports globally; but growth still leans heavily on European demand and rainfall-dependent agricultural output.

- Angola – $152B – resource-driven economy – sub-Saharan Africa’s second-largest oil producer, currently banking windfall revenue from oil prices elevated by the Middle East conflict; diversifying under President Lourenço’s reform program (agriculture, logistics, manufacturing) and anchoring the Lobito Corridor rail project; but oil still accounts for over 90% of exports, leaving the economy structurally exposed to price swings.

- Kenya – $147B – diversifying, reform-oriented grower – East Africa’s commercial and financial hub: fintech, services, tourism, and geothermal power underpin an economy known for M-Pesa’s global lead in mobile money; but public debt has climbed toward 70%+ of GDP, debt service now consumes the majority of government revenue, and the IMF cut its 2026 growth forecast on fuel-cost pressure tied to the Middle East conflict.

- DRC – $123B – resource-driven economy – the continent’s most mineral-rich economy, with cobalt, copper, and lithium reserves feeding global EV and battery demand; it even issued its debut $1.25B Eurobond in April 2026; but per-capita income remains among the lowest on this list, and security instability in the mineral-rich eastern provinces remains a risk to its growth.

- Ethiopia – $122B – diversifying, reform-oriented grower – the fastest-growing economy in Africa in 2026 and the second-fastest growing in the world by real GDP growth (9.2% projected for 2026), driven by hydropower from the Grand Ethiopian Renaissance Dam, Ethiopian Airlines, industrial parks, and agricultural exports, alongside major reforms (currency float, new stock exchange); but the nominal dollar figure is volatile given ongoing debt restructuring and exchange-rate liberalization.

- Ghana – $118B – diversifying, reform-oriented grower – one of the more dramatic turnaround stories here: debt restructuring largely complete, inflation down from above 50% to single digits, sovereign credit rating upgraded five notches from default to ‘B’, and record gold and cocoa export receipts; but debt sustainability risk still assessed as high, and the recovery’s durability depends on continued fiscal discipline.

The diversified industrial & financial hubs have the deepest infrastructure but the least momentum right now.

The resource-driven economies are benefiting from a boom in oil & commodity prices, but continue to face the “resource curse.”

Resource wealth without value creation: The story of Africa’s exports

The diversifying, reform-oriented growers economies aren’t letting current crises go to waste; they’re taking advantage of a convergence of shocks — the Middle East war, the collapse of aid, increasingly untenable debt-service burdens — to make what were previously impractical domestic reforms politically viable.

While economic size and the three categories above tells you where value has accumulated, it doesn’t always tell you where it’s going next.

Decision-makers across the continent and the world trust Afridigest for Africa-focused intelligence & advisory → Afridigest Intelligence

Sign up here to receive the Afridigest newsletter in your inbox.

Share: