Intro

CheckUps is a health benefits platform that delivers virtual and in-person health services on the one hand via CheckUps Medical, and access to healthcare financing and micropayment solutions on the other via CheckUps COVA.

Context

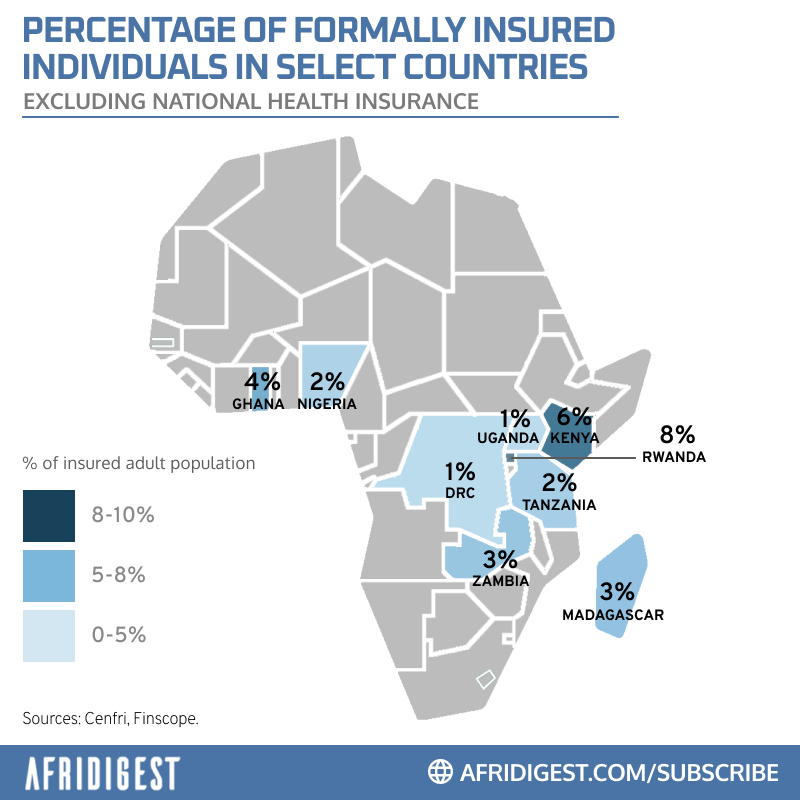

- ‘Financial inclusion’ is on the rise across the African continent, but the vast majority of people with bank accounts still lack private health insurance. In fact, insurance penetration across Africa as a whole is estimated to be under 3%.

- So it’s not surprising that healthcare expenses are a huge burden on households across the continent. According to various researchers, “more than 37% of Africa’s health spending comes from out-of-pocket payments. [And] this burden has significant implications at the household level [with] at least 11% of Africans experiencing catastrophic spending on health care every year, while as many as 38% delay or forgo health care due to high costs.”

- CheckUps allows individuals to access much needed care in a timely fashion with a micropayment & financing solution that unlocks greater benefits and cost reductions than traditional insurance schemes while being less restrictive.

Solution

- The company has two main business units: CheckUps Medical and CheckUps COVA.

- CheckUps Medical is a tech-enabled urgent care platform that leverages a network of freelance dispatch nurses and customer care centers for in-person care.

- CheckUps COVA is a WhatsApp-powered healthcare financing and micropayment solution that facilitates micropayments for medical credits.

- Checkups COVA enables consumers to buy credits for healthcare services directly and also facilitates payments on their behalf from third parties like banks, employers, and family members in the diaspora.

- How it works. Users first enroll on CheckUps via WhatsApp. They can then buy medical credits via mobile money, vouchers, or credit cards, or request a microloan from a bank, MFI, or their employer. They can then use these medical credits to request health benefits and services like lab tests, nurse visits, drug delivery to their homes, and more.

- The company core value proposition is that it offers more bang per buck than alternatives. Specifically, its primary marketing emphasis is that it unlocks $4 of health benefits for every $1 paid.

Revenue/Monetization

- In its traditional home health services business, CheckUps largely generates revenue from the provision of healthcare services where it applies a margin on top of wholesale prices. These include:

- Patients services. Individuals request consultations, lab tests, diagnostic tests, and/or drug delivery at home or at work. The services are billed at retail (cost plus markup) rates. The average revenue per visit is ~$45.

- Pre-employment medical checks. Employers request health checks on potential employees before hiring. The average revenue per check for domestic/household help is ~$76. (ARPC depends on the specific medical review requested by the employer, however. ARPC for commercial food handlers is ~$10, for example.)

- In its micropayments and healthcare financing business, CheckUps generates revenue by enrolling members and encouraging them to make regular micropayments.

- The company is intentionally focused on moving beyond the traditional health revenue streams of consultation, diagnostics, and medication. And it’s now executing its fintech strategy to that end.

- A key part of that strategy is developing a lending marketplace that enables banks and financial institutions to finance healthcare with minimal exposure to outpatient benefits. As this part of the business scales, lead generation and credit-related revenue streams will grow.

Management Overview

- Founders:

- Dr. Moka Lantum (CEO): Three-time healthtech startup founder with an exit. Over 25 years of experience in healthcare financing. Former head of business process improvement and utilization management at Excellus BlueCross BlueShield where he managed $2.2 billion of claims.

- Renee Ngamau (COO): Domain expertise in building solutions that address the needs of African women. Cross-industry operational turnaround experience. Former board chair, Amnesty International Kenya.

Company Overview

- Team Size: 80 full-time, 300 part-time

- Founded: 2018 (before focusing on hybrid fintech-healthtech opportunity in 2022)

- Headquarters: Kenya

- Initial target markets: Kenya and South Sudan (with plans to expand across East Africa in conjunction with partner banks)

- Sector: Healthtech/Fintech

- Early Traction:

- CheckUps has generated over $12 million in revenue in the last 3 years

- Deployed over 400,000 home health dispatches (nurse visits, medication deliveries, etc.)

- Over 30,000 households using the platform over the last 18 months

- Successful integration with a tier 1 banking partner with reach of 4.8 million eligible customers

- Rapidly growing volume and value of daily micropayments

- LTV/CAC ratio of 160 and Net Promoter Score of 86.

Fundraising

- CheckUps has raised $1.9 million (including grant funding) from AAIC, Philips Foundation, and the Lilas Blanc Family Fund.

- The company was also selected to join Visa’s Africa Fintech Accelerator program and the Accelerate Africa program.

- CheckUps is now actively raising $3 million to optimize its platform, finance inventory, and 10x its growth over the next ~36 months. Key drivers of that growth include scaling its network of freelance dispatch nurses and growing its footprint of customer care centers in the markets in which it operates.

Upside/opportunities

- The company is addressing a large market that faces a real problem. While much attention has been paid to healthcare infrastructure and access — i.e., having an adequate supply of hospitals, doctors, and medication — the cost of healthcare remains a significant problem for almost every household in Africa. Over 85% of households across the continent are unable to afford private out-care insurance and a significant opportunity exists in developing sustainable financing solutions for this majority.

- The company has built something that creates real value for users. Unlike traditional insurance, CheckUps COVA doesn’t exclude users due to age or pre-existing conditions, there is no wait time between payment and access to benefits, and the value paid isn’t lost if unused. Moreover, health credits can be distributed and shared with designated beneficiaries in an ‘African-style’ approach that mimics the existing communal method of managing risk. The solution seems to be resonating with early users given a retention rate of over 90%, coupled with healthy gross margins and an attractive LTV/CAC ratio, all suggestive of increasing pull from the market.

- The company is targeting untapped opportunities that might offer an accelerated growth trajectory. The company is targeting ‘non-consumers’ of health insurance and replacing traditional health insurance with a simplified healthcare financing product. Moreover, the CheckUps platform facilitates the participation of African banks in healthcare lending opportunities — a sector that has seen minimal bank participation at the non-infrastructure level to date. If all goes well, the company’s growth in these untapped, new markets could be much faster than in already existing markets with higher levels of competition.

Downside/risks/questions

- Can the company crack the enterprise G2M? The enterprise sales model — e.g., getting banks on board to provide financing for CheckUps COVA — is key to the company’s ability to reach venture scale in a reasonable time frame. But this involves risks relative to the sales cycle, building and incentivizing the right sales team, and the overall enterprise sales process. As it has only recently began executing its enterprise strategy, CheckUps doesn’t have much of a track record here yet. That said, to the degree that banks are looking for alternative ways to deploy capital, CheckUps’ solution might be welcomed by them.

- What are the drivers of defensibility? CheckUps COVA is an early mover in the health financing space that’s providing an alternative to traditional health insurance. While incumbents may have overlooked the market opportunity in the past, if CheckUps COVA proves it out, other market participants might be quick to move into the space. A potential source of defensibility is a proprietary algorithm based on millions of data points that allows for forecasting and optimization of benefits allocation, but this and other potential drivers of defensibility are worth further reflection.

- How significant are potential regulatory risks? CheckUps is operating at the intersection of two heavily regulated sectors: healthcare and fintech. While there seems to be minimal risk today, the potential for regulatory challenges and pushback from powerful incumbents on both the CheckUps Medical and CheckUps COVA businesses will increase as the company scales.

Competitors/Comparable Companies

- Healthcare financing fintechs: e.g., ClinicPesa

- Financial services institutions offering microinsurance schemes: e.g., Equity Bank’s Equimed and Equihealth

- Insurtechs providing health microinsurance plans: e.g., Turaco, BIMA

Hear from the founders in their own words

Last word

CheckUps offers an innovative, value-additive approach to healthcare financing and delivery in a market replete with healthcare challenges. The company deploys a unique model that combines healthcare financing and micro-payments (CheckUps COVA) with in-house end-to-end delivery of healthcare services (CheckUps Medical).

The company’s founding team — led by an MD/PhD medical doctor — has relevant domain expertise and over two decades of experience in healthcare financing. And it’s used its insights earned over the years to great effect in recent times. Over the last 18 months in particular, the company has demonstrated promising results that are suggestive of significant latent potential and product-market fit.

That said, rather than capturing existing customers or markets, the company is effectively focused on creating new consumers and new markets — a very high risk/reward approach.

What do you think?

Would you write a check for CheckUps?

Disclaimer: Nothing in this post constitutes investment advice. Conduct your own research, perform due diligence, and/or consult with investment advisers before making investment decisions.

Share: