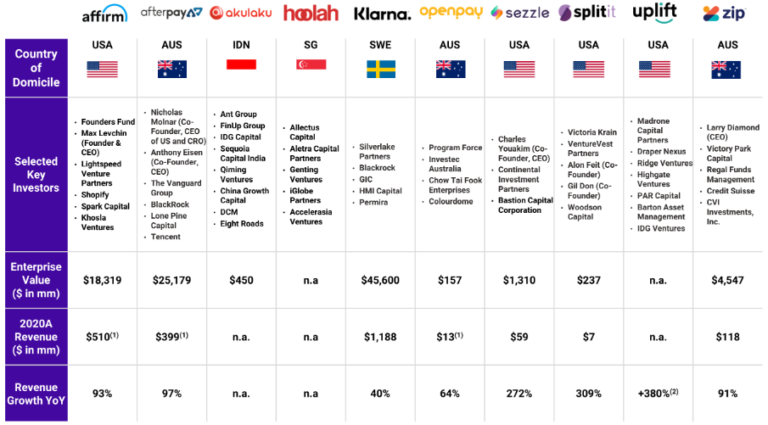

Over the last few years, ‘buy now, pay later’ (BNPL) has taken off worldwide and produced a number of global juggernauts like Klarna — once one of the world’s most valuable fintechs.

Source: FT Partners. July 2021.

BNPL in Africa

Across Africa, BNPL solutions are increasingly common across the continent’s major tech hubs too, with offerings from Lipa Later, Aspira, Safaricom, and others in Kenya; Carbon, CredPal, Klump, and others in Nigeria; Shahry, ValU, MNT-Halan, and others in Egypt; and PayFlex, PayJustNow, Float, and more in South Africa.

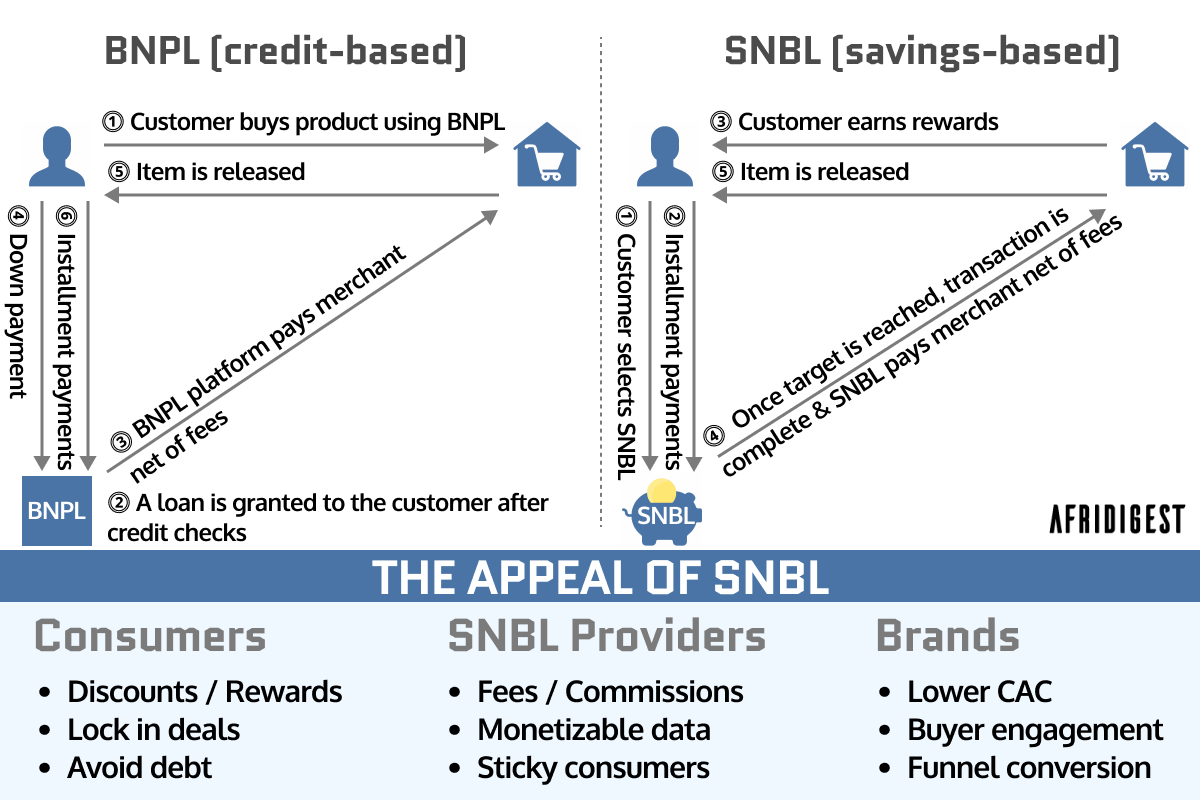

The typical BNPL model gives customers instant access to an item after a credit check and a 20-25% down payment, with the outstanding balance split into multiple equal installments payable over a pre-defined time period.

And while some BNPL providers don’t charge interest, many do, and most platforms charge substantial penalties for late payments.

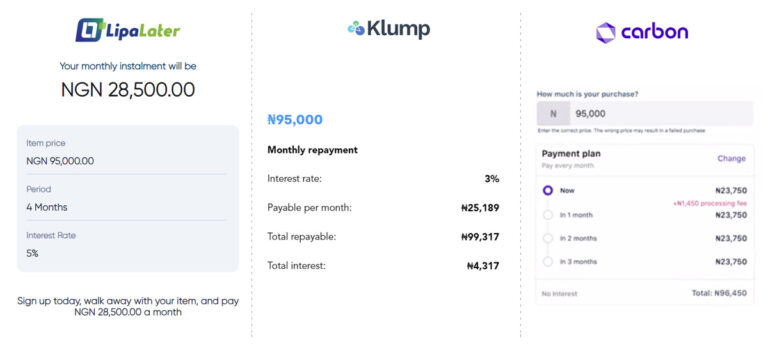

Terms for a NGN95,000 BNPL purchase paid over 4 months at LipaLater, Klump, and Carbon in Nigeria.

But despite the rapid adoption of BNPL globally, today there are an increasing number of questions about the sustainability of the model. Klarna, for example, saw its valuation cut 85% from ~$46 billion in June 2021 to ~$7 billion in June 2022 as losses tripled.

Against that backdrop, there’s a new breed of innovators who view BNPL and related credit-driven models as undesirable; they argue that, aside from questions of commercial viability, these models lead to impulse-driven overspending, debt traps, and other negative outcomes.

So they’re innovating around savings and embedding new functionalities into the online retail experience.

The sector’s called ‘save now, buy later’ (SNBL). And it’s exactly what it sounds like.

Save now, buy later across developed & emerging markets

Unlike the BNPL model where consumers pay a down payment and receive the item immediately, under SNBL models, consumers choose an installment plan and make payments, but generally don’t receive the item until they’ve paid the full purchase price.

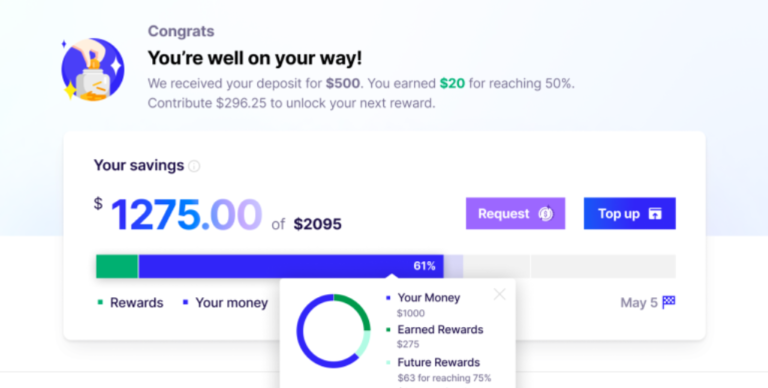

Perhaps the leading player in the SNBL space globally is America’s Accrue Savings which raised a $25 million Series A led by Tiger Global last year.

The company partners with brands to embed SNBL solutions at checkout and monetizes via card interchange fees and performance fees from brand partners. And as customers reach certain savings milestones, they earn cash rewards from those brands, reducing the purchase price of desired items. When there’s enough money saved, the transaction is completed, but if for any reason the customer has a change of mind before then, he/she can withdraw the funds deposited at no additional cost (minus cash rewards added by retailers).

Source: Accrue Savings. 2022.

Other players in the SNBL space globally include Austria’s Monkee and British women-focused savings platform Cashmere.

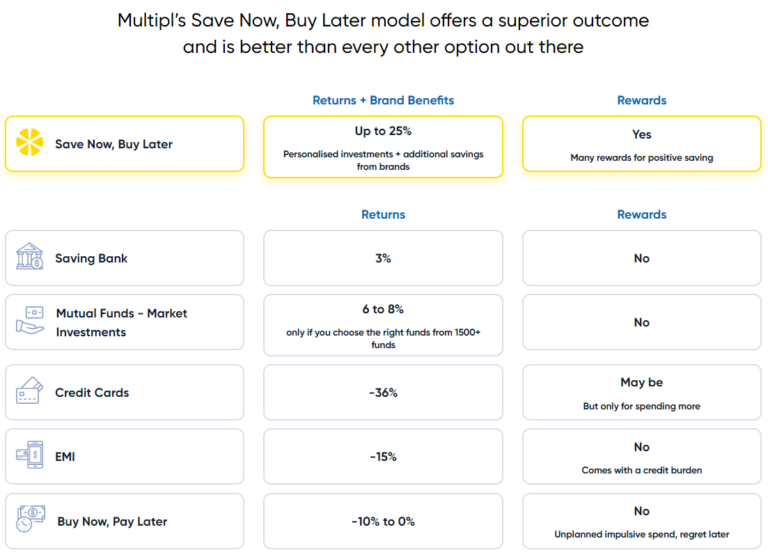

And across emerging markets specifically, the model seems to be currently enjoying the most traction in India, with offerings from Tortoise, Hubble, Multipl, and others leading the way.

Tortoise offers merchant-embedded BNPL solutions similar to Accrue; Hubble offers consumers interest on amounts saved in its digital wallet and discounts on purchases made through the platform; and Multipl, an investment platform, allows users to save directly with brands and receive cash rewards.

Source: Multiple. 2023.

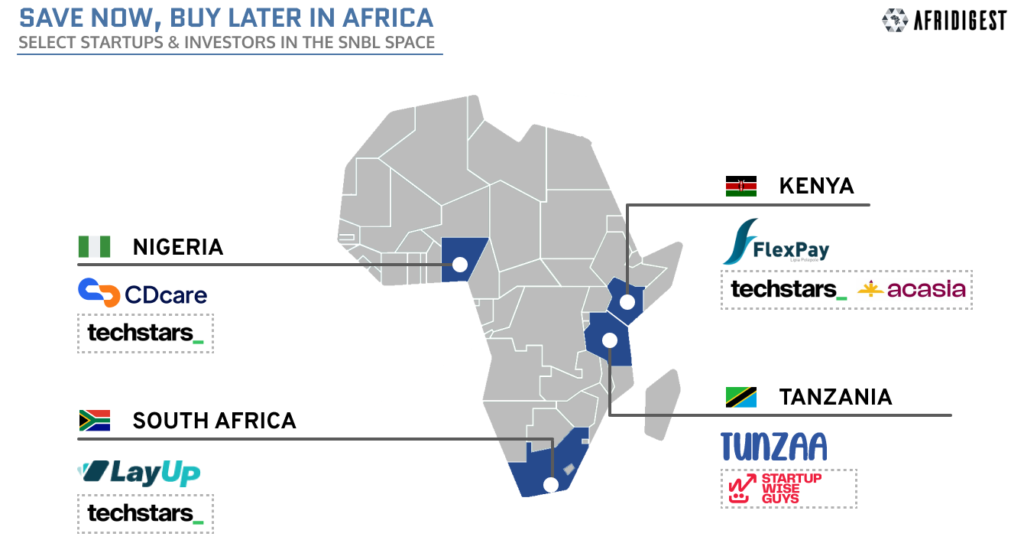

Across Africa, while there’s a long history of installment savings schemes, the modern SNBL sector is nascent.

Some of the players leading the charge across the continent include Kenya’s FlexPay which received an investment from acasia (formerly the Cairo Angels Syndicate Fund) last year and previously participated in the Barclays Cape Town Techstars program, Tanzania’s Tunzaa which participated in the Startup Wise Guys accelerator last year, South Africa’s LayUp which participated in the Barclays Cape Town Techstars program several years ago, and Nigeria’s CDcare which participated in the most recent ARM Labs Lagos Techstars program.

CDcare, a Nigerian platform leveraging a hybrid SNBL model

CDcare is a bit of a hybrid player.

Source: CDcare. 2023.

Unlike pure SNBL options, it allows users to receive items before the full price is paid, thus incurring some credit risk. But unlike typical BNPL models, delivery happens after 50% or more of the purchase price is paid, not with the initial down payment.

It’s also unique in another sense. Unlike many SNBL providers that partner directly with brands and generate revenue via commissions, CDcare works with wholesalers and distributors to acquire inventory at low prices and it generates revenue via a retail markup.

It’s a model that appears to be working well. Over the twelve-month period from February 2022 to January 2023, the company sold $6 million worth of goods with gross margins of 10-15% and a default rate of just 0.4% — and that’s with no external debt raised.

Below is an edited version of our conversation with CDcare’s Tobi Odukoya.

Tobi Odukoya, CEO & Co-Founder, CDcare

Tobi, we talked a bit about Nigeria and African markets being savings-first. Can you share a bit more about that? What’s your perspective on the consumer reception to credit?

I have firsthand experience with the savings-first culture in Africa. In my university days, I ran a “loan-a-laptop” business that failed due to consumer reluctance to pay interest. I noticed then that many Nigerians would rather save up for purchases than take on credit, even at minimal interest rates, due to various cultural and religious beliefs.

While there’s no doubt a growing demand for credit in Nigeria and other African markets, it’s essential to offer it in a way that aligns with local values and ways of life. Nigeria has a significant Muslim population, and any interest-bearing credit company has already limited itself to less than 50% of the available market, for example.

I agree with Chijioke Dozie, Co-Founder of [Nigerian credit-led digital bank] Carbon, who recently stated, “There isn’t a big culture of credit [in Africa], and that’s one thing we want to change.”

But rather than trying to change market norms, at CDcare, we’ve built a solution that aligns with the prevailing culture and beliefs of most Africans. As the saying goes, “Culture eats strategy for breakfast.”

What are some of the problems you see with existing BNPL models?

It’s not a profitable business in Africa. The higher the ratio of retail margin to interest rate (retail margin / interest rate), the higher the chance for traditional BNPL to work and be profitable. In America and other markets where BNPL is popular, the ratio is above 1, while for most African markets the value is below 1. Wherever the value is below 1, BNPL providers will struggle to cover operational costs and service their debt.

Please describe CDcare’s model.

CDcare operates a save-now-buy-later model. Since Africans would rather save than borrow, we allow them to save an amount weekly or monthly towards needed items. And once they’ve paid 50% of the purchase price, the item is delivered. We sell items at or below market prices, and we don’t charge any form of interest. We’re also very conscious of customers with low purchasing power, and we provide longer duration spreads for convenience and accessibility.

At the end of the day, we provide an alternative to traditional credit-based consumer financing models that aren’t well-suited for the African market. Our approach not only helps customers avoid debt but also fosters a culture of saving, which is essential for long-term financial stability.

Some zero-interest BNPL models exist in the market; why would a consumer choose CDcare instead of one of these options?

- Many people would rather save than borrow, and CDcare allows them to do that easily and flexibly while avoiding any hidden and/or late fees.

- Most zero-interest schemes have hidden costs. For example, product prices are often marked up to make up for the cost of debt financing and high operational costs. And consumers are more aware of these things than many companies realize.

- Many zero-interest BNPL schemes have high eligibility requirements that discourage many customers.

- And they also tend to have low loan limits, while most BNPL purchases are for big-ticket items.

Do you think there’ll be more platforms exploring SNBL models as opposed to BNPL models across Africa? Why or why not?

This is going to be the winning model in Africa, and I expect there’ll be new players entering the space based on our success.

Many thanks for your time, Tobi!

Afridigest’s advisory arm Afridigest Intelligence helps executives, investors, and institutions create and capture opportunities across African markets through strategic intelligence, analysis, and insight. Contact intelligence@afridigest.com to see how we can help.

Share: